Divorce Financial Specialist Case Study – The Jones Family

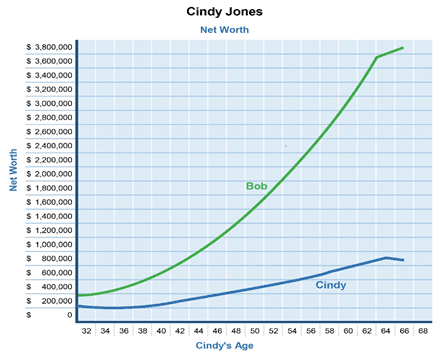

Net Worth Analysis

Net Worth Analysis Notes: Based on the father’s proposed settlement, this is the projected long-term financial future of both parties.

The green line represents the father, and the blue line represents the mother.

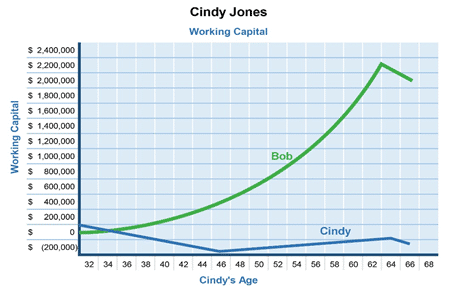

Working Capital Analysis

Working Capital Analysis Notes: Her case seems to be worse than illustrated in the net worth graph. She starts with a negative cash flow of $19,504 in the first year because her expenses exceed her income. The mother begins with the working capital amount of $76,425. By the third year, it will be down to $2,485 to cover her costs. Once the working capital is gone, she must withdraw from her retirement accounts. By age 36, her total spendable assets will be exhausted.

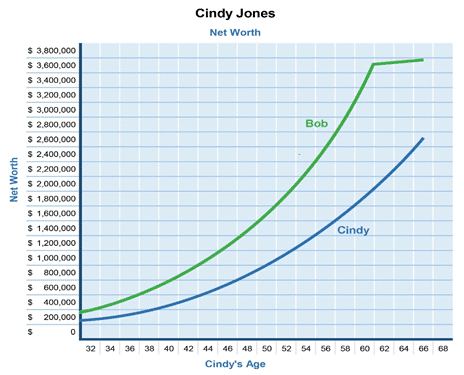

Revised Net Worth Analysis

Revised Net Worth Analysis: A few changes in distributing assets can create a much more equitable financial future for both. His net worth has not been affected, but hers has increased significantly. Now let’s look closely at the working capital.

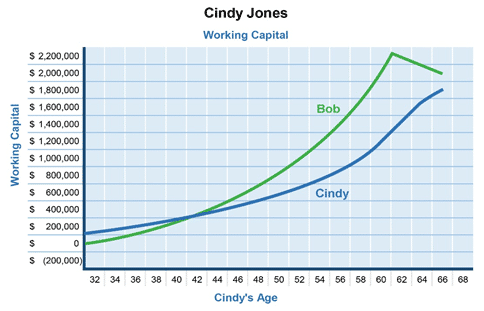

Working Capital Analysis: His working capital has changed little from the initial proposal. Her wealth has increased substantially. By selling off the matrimonial home and moving into a rental, the mother reduces her expenses to $30,050 per year. She’s also reduced her mortgage payments. Also, there’s an increase in working capital from the increase in spousal support and the proceeds from the house. And she doesn’t need to withdraw from her retirement accounts to cover her expenses, so they’ll grow to more than $230,000 by the time she retires. This creates financial independence for both parties into the future.

Ken Maynard CDFA, Acc.FM

I assist intelligent and successful couples in navigating the Divorce Industrial Complex by crafting rapid, custom separation agreements that pave the way for a smooth transition towards a secure future. This efficient process is achieved in about four meetings, effectively sidestepping the excessive conflicts, confusion, and costs commonly linked to legal proceedings. Clients have the flexibility to collaborate with me either via video conference or in-person through a DTSW associate at any of our six Greater Toronto mediation centers, located in Aurora, Barrie, North York, Vaughan, Mississauga, and Scarborough.